What Is eSAF? The Complete Guide to

Electro-Sustainable Aviation Fuel in 2026

Definition · How it’s made · ReFuelEU mandates · Production gap · Costs · Key players · 2030–2050 outlook

eSAF — electro-Sustainable Aviation Fuel — is the most strategically important fuel in European aviation policy. It is the only pathway that can meet ReFuelEU’s long-term mandates, decarbonise long-haul aviation without electrification, and be produced entirely from renewable energy without biomass constraints. Yet in 2024, it represented a fraction of a percent of global jet fuel. This guide explains everything: what eSAF is, how it is produced, what the mandates require, how far supply falls short, what it costs today and what the road to 2050 looks like.

What Is eSAF? — The Simple Definition

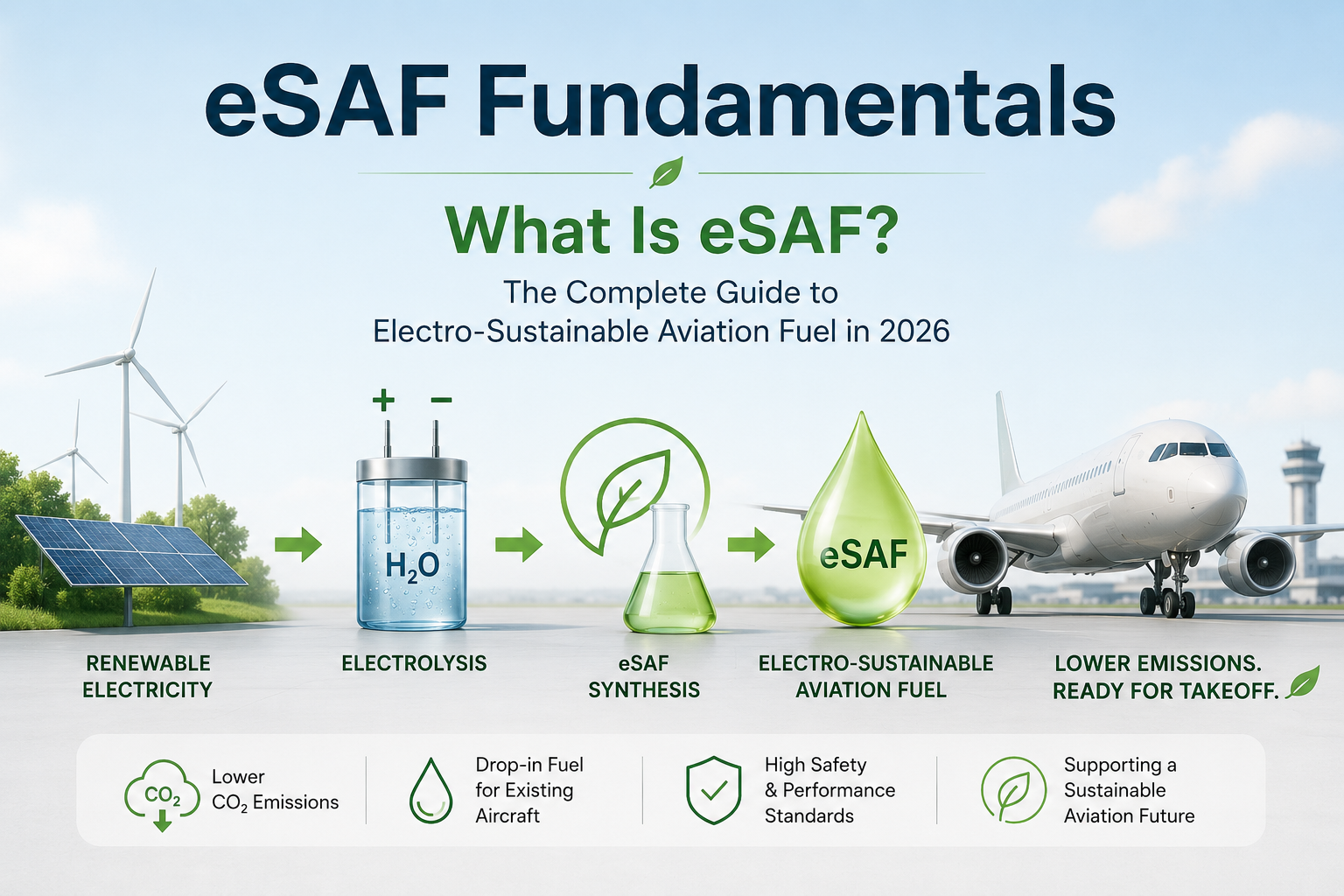

eSAF (electro-Sustainable Aviation Fuel) is jet fuel produced from renewable electricity, green hydrogen and captured CO₂ — with no fossil fuels involved at any stage of production. It is chemically identical to conventional jet fuel and works in all existing aircraft without any modification.

The “e” stands for electro — referring to the renewable electricity that powers the entire production chain. This distinguishes eSAF from bio-based SAF (produced from waste oils, agricultural residues or municipal solid waste), which relies on limited biological feedstocks.

SAF (Sustainable Aviation Fuel) = broad category covering ALL non-fossil aviation fuels including bio-based pathways (HEFA from waste oils, AtJ from ethanol, FT from biomass gasification) AND eSAF.

eSAF (electro-SAF) = the specific sub-category produced from renewable electricity + H₂ + CO₂ via Power-to-Liquid. It is what ReFuelEU’s specific eSAF sub-mandate targets: 1.2% by 2030, 35% by 2050. HEFA and other bio-SAF count toward the general SAF mandate but NOT toward the eSAF sub-mandate.

This distinction is legally critical: fuel suppliers who supply HEFA-only meet the general SAF mandate but still face penalties for missing the eSAF sub-mandate.

How eSAF Is Produced — The Power-to-Liquid Process

eSAF is produced via Power-to-Liquid (PtL) technology — a multi-step electrochemical and thermochemical process that converts renewable electricity into liquid hydrocarbon fuel.

Renewable electricity from solar, wind or hydro

Electrolysis splits water → green hydrogen H₂ + oxygen

CO₂ captured from air (DAC) or industrial sources

H₂ + CO₂ → syngas via RWGS · then Fischer-Tropsch synthesis → wax

Wax upgraded to eSAF drop-in jet fuel · ASTM certified

ReFuelEU Aviation — The eSAF Mandate in Detail

ReFuelEU Aviation (EU Regulation 2023/2405) entered into force on 1 January 2024 and applies to all flights departing from EU airports. It sets binding minimum SAF blending requirements for aviation fuel suppliers — with a specific sub-mandate for eSAF (synthetic fuels only).

As of 1 January 2026, Switzerland has also adopted the ReFuelEU Aviation Regulation, meaning aviation fuel suppliers at Zurich and Geneva airports must also ensure a minimum 2% SAF blend, ramping up to 70% by 2050.

The Production Gap — The Central Challenge of the Decade

The most critical challenge facing the eSAF industry is the gap between what mandates require and what plants can actually produce. The numbers are stark.

⚠ Pipeline figures assume all 41 EU large-scale projects reach FID — as of June 2025 none had. Source: Transport & Environment report June 2025 — research, not guaranteed production figures.

“SAF production growth fell short of expectations as poorly designed mandates stalled momentum in the fledgling SAF industry. If the goal of SAF mandates was to slow progress and increase prices, policymakers knocked it out of the park.”

Willie Walsh — Director General, IATA IATA Global Media Day, Geneva, December 9, 2025 — official statementSAF prices exceed fossil-based jet fuel by a factor of two, and by up to a factor of five in mandated markets. The growth rate for SAF production is slowing down — while SAF output is expected to hit 1.9 Mt in 2025, growth is projected to crawl to 2.4 Mt in 2026, reaching only 0.8% of jet fuel consumption.

eSAF Costs — Where Are We Today?

eSAF is expected to be commercialised after 2030 and more widely available post 2040. Renewable energy costs have dropped 90% in the last decade, and with these costs expected to continue decreasing alongside innovations in carbon sourcing — securing carbon monoxide from existing industrial sources instead of processing CO₂ from the atmosphere helps cut energy costs by around 30% — it is feasible that eSAF could reach cost parity with other jet fuels.

Key Players in eSAF Production 2025–2026

Europe’s first commercial-scale eSAF plant. ERA ONE (Frankfurt-Höchst): 2,500 t/yr from biogenic CO₂ + green H₂. Financed by BEI + Breakthrough Energy Catalyst (€70M). Next target: 35,000 t/yr. Normandy plant (France) with TERTU via T.H2 JV (March 2026).

Project Roadrunner: 23,000 t/yr eSAF in West Texas. FID reached June 2025, construction started. Renewable wind + CO₂ capture. Amazon confirmed customer. IRA tax credits ($3/gal). Largest eSAF facility in the Americas.

Mosjøen PtL facility: 50 million litres of eSAF by 2026, scaling to 250 million litres by 2030. Uses Norwegian hydropower (100% renewable) for electrolysis. One of Europe’s most advanced PtL projects at near-commercial scale.

Haru Oni (Chile, Porsche-backed): world’s first commercial e-fuel production, including aviation fractions. Project Roadrunner (Texas): large-scale eSAF. Secured $164M from Idemitsu Kosan. Pioneer of commercial PtL globally.

World’s largest SAF producer overall (HEFA pathway). 1.5 Mt/yr total SAF capacity (Rotterdam + Singapore + Finland). Investing in PtL eSAF for post-2030. Currently supplies the majority of European SAF market.

Unique solar-to-liquid pathway: concentrated solar power drives Fischer-Tropsch synthesis. DAWN plant (Germany): world’s first industrial solar fuel facility. eSAF produced directly from sunlight + CO₂ — no electrolysis step needed.

eSAF Outlook 2026–2050 — What Needs to Happen

It is estimated that 104 to 106 additional SAF plants need to be built in the EU by 2050 to cater for the necessary alternative aviation fuel production capacity — of which around 40 large-scale e-fuel projects are already planned in Europe, with a potential production capacity close to 3 million tonnes.

Three things need to happen simultaneously for eSAF to meet its mandates:

1. Green hydrogen costs must fall below €2/kg. At current costs of €4–8/kg, eSAF is uncompetitive. The IEA targets sub-€2/kg green hydrogen by 2030 through electrolyser scale-up — this is the single most important cost lever.

2. FIDs must be secured for large-scale plants by end of 2026. Given 3–4 year construction timelines, any FID beyond early 2027 means the 2030 eSAF sub-mandate cannot physically be met from European plants alone.

3. Regulatory clarity must be maintained. The Industrial Accelerator Act unveiled 4 March 2026 will contribute to scaling green hydrogen through a “Made in Europe” proposal extending to electrolysers, with easier permitting for e-fuel projects and the creation of green lead markets. This is the right direction — but implementation speed matters.

🔗 Also explore: e-fuels.ai — EU e-fuels regulation · syntheticfuels.ai — global synthetic fuels market · syntheticfuelsmarket.ai — market data · safaviation.eu — SAF aviation portal

ReFuelEU mandate data: European Commission official (transport.ec.europa.eu) · EASA Sustainable Aviation Fuels page (easa.europa.eu) · ReFuelEU Aviation Regulation EU 2023/2405 — all official.

Production gap & FID data: Transport & Environment report “The e-SAF market: Europe’s head start and the road ahead” (June 2025, uploads.transportenvironment.org) · Climate Catalyst alternative aviation fuel policy analysis (March 2026) — research.

IATA data & quotes: IATA Global Media Day press release, Geneva, December 9, 2025 (iata.org) — official.

Cost data: Air bp “What is eSAF” (bp.com) · EASA reference prices Feb. 2025 · Plane Sight News (January 2026).

T&E economic analysis: NEG8 Carbon citing Transport & Environment 2026 analysis (neg8carbon.com, May 2026).

Industrial Accelerator Act: Climate Catalyst (March 2026) — official EU document reference.

Switzerland ReFuelEU adoption: European Commission official (January 2026).

Key player data: INERATEC official · Infinium official · Norsk e-Fuel official · HIF Global official · Neste IR · Synhelion official.

Disclaimer: Documentary portal. All data from named independent sources as cited above. Not investment advice. Regulatory data subject to change — always verify with official sources. BESS Energie SRL · BCE 0698.949.732 · Heusy (Verviers, Belgium) · info@bess.be · e-saf.ai